CERTIFICATE OF INCORPORATION OF SBAA INCORPORATED

(Under Section 402 of the Not-for-Profit Corporation Law of NY State)

FIRST: The name of the Corporation is: SBAA INCORPORATED (SBA3.ORG)

SECOND: The Corporation is a corporation as defined in subparagraph (a)(5) of Section 102 of the Not-for-Profit Corporation Law of the State of New York.

THIRD: The non-business and non-pecuniary purposes of the Corporation are as follows:

To effectively advance the interest of low income Asian-Americans residing in or doing business in NY; and to unite, aid, assist, and help low-income Asian-Americans in NY.

To hold social gatherings and meetings to form enduring friendships among them; to hold seminars and forums open to the general public so that low income Asian-Americans freely exchange information and discuss current matters; to provide marketing ideas, business tips, and immigration information to low income Asian Americans residing or doing business in NY; to gather food, clothing, and other basic necessities for those communities that have been affected by natural disasters; and to provide financial support to children and senior citizens from lowincome Asian-American families.

To do any other act or thing incidental to or connected with the foregoing purposes or in advancement thereof, but not for the pecuniary profit of financial gain of the directors or officers of the Corporation. However, nothing herein shall authorize this corporation, directly or indirectly, to engage in or include among its purposes, any of the activities entioned in the Not-for-Profit Corporation law, Section 404 (a)-(w).

FOURTH: The corporation is organized and empowered:

a. To make charitable contributions.

b. To conduct, engage, promote and assist in a campaign or campaigns, and any efforts

whatsoever, for the collection and raising of funds, and to solicit appeal for, and

request monies, funds, securities, donations, pledges and property of every nature

whatsoever, exclusively for charitable purposes.

c. To use or donate the whole or any part of the monies, funds, securities, donations,

pledges and property of every nature whatsoever and the income there from

exclusively for charitable purposes.

d. To do any and all acts and things, and to exercise any and all powers which may now

or hereafter be lawful for the corporation to do or exercise under and pursuant to the

laws of the purposes of the corporation.

e. Subject to the limitations prescribed by stature and in furtherance of its corporate

powers which shall not be deemed to be exclusive of any other powers provided by

law: To solicit, collect, accept, hold, invest, reinvest and administer any gifts,

bequests, grants, contributions, benefits of trusts (but not to act as trustee of any trust)

and property of any sort, without limitation as to amount or value, from the public

generally.

The corporation shall have all general powers enumerated in Section 202 of the Not-for-Profit Corporation Law, together with the power to solicit grants for contributions for corporate purposes.

FIFTH: As defined in Section 201 of the Not-for-Profit Corporation Law, the Corporation is a: Type A Corporation

… …

SEVENTH: The Office of the Corporation is to be located in New York State and in: Nassau County

EIGHTH: The Secretary of State of the State of New York hereby is designated as the agent of the Corporation upon whom process in any action or proceeding against the Corporation may be served. The post office address to which the Secretary of State shall mail a copy of any process against the Corporation, served upon the Secretary of State, is: 55 Northern Blvd., Great Neck, NY 11021

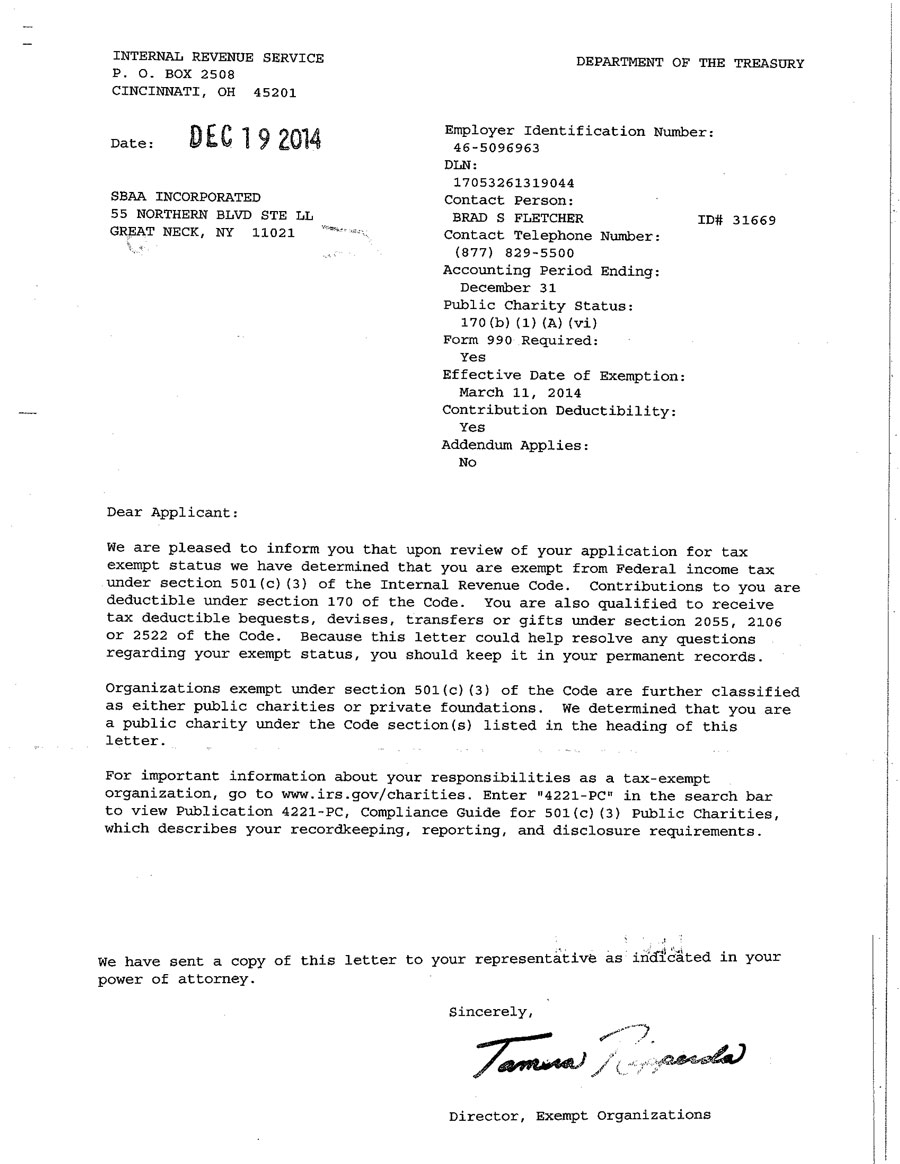

NINTH: IRS Clause: The corporation is organized exclusively for charitable, religious, educational, and scientific purposes, including, for such purposes, the making of distributions to organizations that qualify as exempt organizations as specified under Section 501 (c)(3) of the Internal Revenue Code of 1954, and shall not carry on any activities not permitted to be carried on by a corporation exempt from Federal income tax under Internal Revenue Code Section 501 (c)(3) or corresponding provisions of any subsequent Federal tax laws or by a corporation, contributions to which are deductible under Section 170 (c)(3) of the Internal Revenue Code of 1954 (or the corresponding provision of any future United States Revenue Law).

TENTH: No part of the net earnings of the corporation shall inure to the benefit of any member, trustee, director, officer of the corporation, or any private individual (except that reasonable compensation may be paid for services rendered to or for the corporation), and no member, trustee, officer of the corporation or any private individual shall be entitled to share in the distribution of any of the corporate assets on dissolution of the corporation.

ELEVENTH: Upon the dissolution of the Corporation, assets shall be distributed for one or more exempt purposes within the meaning of section 501(c)(3) of the Internal Revenue Code, or corresponding section of any future Federal tax code, or shall be distributed to the federal government, or to a state or local government, for a public purpose.

TWELFTH: No substantial part of the activities of the Corporation shall be carrying on propaganda, or otherwise attempting to influence legislation (except as otherwise provided by Internal Revenue Code Section 501 (h), and the corporation shall not participate in or intervene (including the publication or distribution of statements), any political campaign on behalf of or in opposition to any candidate, or participating in, or intervening in (including the publication or distribution of statements), any political campaign on behalf of any candidate for public office.

THIRTEENTH: In any taxable year in which the corporation is a private foundation as described in IRC Sec 509(3), the corporation shall distribute its income for said period at such time and manner as not to subject it to tax under IRC Sec 4942, and the corporation shall not (a) engage in any act of self-dealing as defined in IRC Sec 4941(d), retain any excess business holdings as defined in IRC Sec 4944(c), (b) make any investments in such manner as to subject the corporation to tax under IRC Sec 4944, or (c) make any taxable expenditures as defined in IRC Sec 4945(d) or corresponding provisions of any subsequent Federal tax laws.

…. …

Leave a comment